There are a lot of things to think about when considering to buy a new house. It is a BIG decision, a big investment and, considered by many to be an even bigger commitment than marriage. Here at Sell House Fast we buy any house, but as a private buyer, you can afford to be (and should be!) a lot more fussy. You can relocate if you really are not happy with your choice. But the buying process is invariably long and can be highly expensive if you choose to sell through an estate agent; so you must think carefully.

Here is your house buying checklist:

1. Is house buying right for you?

House prices are on the rise and they have finally got back to pre-recession levels with the average property value in England & Wales sitting at £181, 619. There has also been a 12.5% rise in typical rent prices across the UK, so you really need to crunch the numbers before deciding whether house buying is better than renting or even renting to buy, right now.

2. Is this your first time buying?

If you are lucky enough to be house buying for the first time, then this is a very exciting, but also very challenging time to be getting on the property ladder. Nevertheless, the government and banks alike have been hard at work creating solutions for new buyers. There is the help-to-buy scheme that allows buyers to take a mortgage with 5% deposit and borrowing a higher loan-to-value mortgage than average, with a help-to-buy ISA planned to be released in December this year. Many banks have incentives for first-time buyers with lower initial interest rates or rewards.

3. Are you buying alone or with someone else?

Houses are not cheap, so splitting the costs of a property between a partner or your friends and family can be a great solution to getting on the property ladder quicker. If you choose to do this you must decide whether you all own a specific share in the property or not. The first is a Tenants in Common ownership and the latter a Beneficial Joint Tenants ownership.

4. Can you accumulate the mortgage deposit?

Depending on how much you can afford to invest in a deposit upfront, the consequent interest rate a bank can offer will vary. The higher the initial payment i.e. 20%+ will ensure a much better interest rate.

5. What type of mortgage is right for you?

There are many mortgage options to suit different budgets, with standard repayment mortgages that are fixed at an initial interest rate for a fixed term period e.g. 2-5 years. There are variable rate loans which vary under the lenders discretion, not necessarily with the Bank of England base rate and variable mortgages that do track either the BoE base rate or another similar rate which are called tracker mortgages. There are interest-only options and a combination of both interest and repayment. And if you are buying to let, there are mortgages for that too with usually higher interest rates. Use the UKMortgages and mortgage mentor app to make comparisons, calculate and analyse the best deal for you.

6. What area do you want to live in?

Choosing the ideal location for your new home is the first step for many prospective buyers. Things to consider are; crime rates, neighbourhood, schools, flooding statistics, nearby sales data etc. There are many house-buying apps on the market to help in every aspect, you can even find out how close your nearest celebrities are with Celebrity Planet. There is also a wealth of information available online from council tax bandings to school reports, air quality and your nearest mobile phone mast.

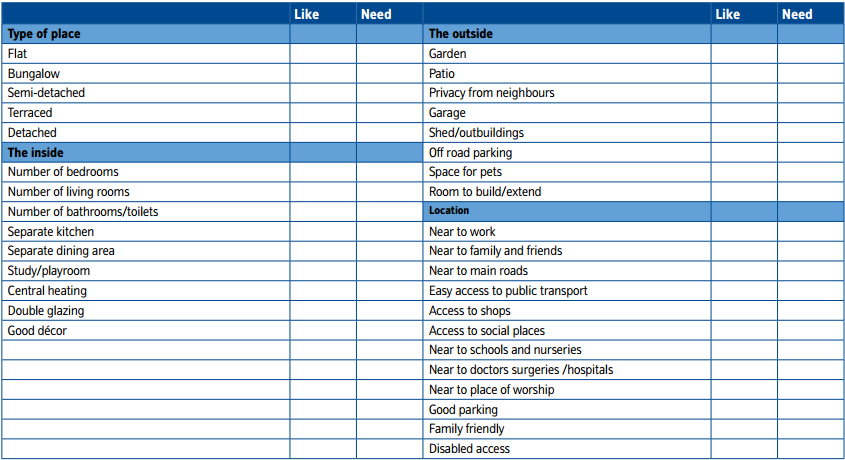

7. What do you need?

What are the essentials of your new investment? Ask yourself what your necessities are and work upwards from there to drill down your property search. Two beds or three, detached or semi-detached, driveway or nearby train station. Create a ‘would like’ and ‘need’ list if it helps to decide.

Source: Nationwide.co.uk, Home Buyers’ Guide

8. Optimise your credit score

If you’ve got the money and found the home of your dreams then you don’t want your credit score to be the only thing standing between you and your sanctuary. Check your credit score before applying for any mortgages, accounts registered in your name to the wrong address could mean rejection. So be pedantic and be thorough with your credit files to boost the chances of securing a mortgage.

9. Car or commute?

Some people move house to be closer to work to avoid congestion and busy traffic. But does this necessarily equate to a saving? With property prices in London averaging £481, 820, it is certainly cheaper to sit on the Overground into the capital than having the underground on your doorstep.

10. Consider the time of year

Spring marks the start of the ‘property-buying’ season with Grand Designs presenter, Kevin McCloud touting May to be “a good time to look around as the leaves are not on the trees and you can know what’s at the bottom of the garden.” He also recommends Google Earth as a great tool for peering into neighbourhoods and researching an area.

11. How much will it cost to run?

People are becoming more and more eco-conscious with insulated homes fetching a premium over similar less insulated properties. A well-insulated home will save you hundreds or even thousands in energy bills. Be sure to query the type of boiler and check its efficiency, check windows are double glazed or triple glazed, also ask about loft and wall insulation.

12. What are the steps in buying?

It’s not as simple as ‘getting a mortgage’, making an offer and picking up the keys. Here is how house-buying works:

- House buying with someone else? Consider your ownership options

- Conduct a property search

- Attend house viewings

- Calculate your budget

- Obtain an Agreement in Principle from your chosen lender (which is basically a green light that they will lend you your chosen amount)

- Make an offer

- If the offer is accepted get a surveyor’s report completed and have your solicitor to check legal issues

- Pay your deposit

- Exchange contracts

- Complete the deal by transferring the rest of the funds and collecting your keys and deeds. You are now legal owner, the house is yours.

Feature image credit: Billion Photos/Shutterstock